Maryland CPA CPE Requirements [Updated 2026]

- Braden Norwood

- Feb 3, 2021

- 3 min read

Updated: Jul 2

Last Updated: April 27, 2026

Overview of Maryland CPA CPE Requirements

CPE is the main way the AICPA makes sure its members comply with regulations. But even more, it helps individuals offer exemplary service to clients and businesses. However, not all CPAs have to meet the same standards when it comes to obtaining CPE credits. Because each state's Board of Accountancy sets its own stipulations and limitations for CPE. And this means the Maryland CPA CPE requirements also differ from other places. So, CPAs should thoroughly research and understand the state requirements set for their location before starting the license renewal process. Otherwise, they may find they've failed to meet the right conditions.

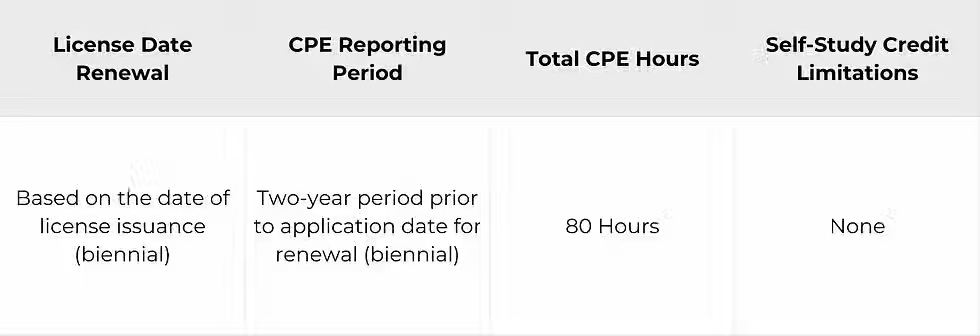

AICPA members in Maryland must renew their license every two years. And during that time, have to complete 80 hours of CPE. Listed in the chart below are some of the primary recertification objectives and limitations.

Share this Image On Your Site

<p><a href="https://vtrpro.com/blog/news-and-articles/cpa-cpe/maryland-cpa-cpe-requirements-to-renew-a-license/"><img src="https://assets.vtrlearning.com/wp-uploads/2021/02/Maryland-CPA-CPE-Requirements-Overview-1024x768.png" alt="Maryland CPA CPE Requirements" /></a></p>

Subject Area Requirements

During each two-year recertification period, 4 of the required 80 hours have to cover subjects dealing with Professional Ethics. There are no further subject area requirements for licensees in Maryland.

Credit Limitations and Calculation

CPAs who instruct or offer formal presentations can earn up to 45 hours of CPE credit per renewal period. Here, for first-time presentations, each hour spent instructing will afford three credits. However, repeat presentations of the same material will afford no credit within the same renewal cycle.

CPAs who are instructors at an accredited college or university can also claim recertification credit for instruction. But this method is limited to 15 CPE hours per semester hour and 10 CPE hours per quarter hour. Likewise, CPAs who are currently participating in college or university courses can claim CPE credit hours. Similarly, these equal 15 CPE hours per semester hour or 10 CPE hours per quarter hour.

CPAs can also obtain credit if they have authored and published any material of an educational or instructional nature. This type of credit may not exceed 10 hours per published article. Furthermore, CPAs can only earn a maximum of 40 hours in any given reporting period.

For instances of peer review, credits cannot exceed 16 hours. Furthermore, peer reviewer may allocate a maximum of 12 hours for an engagement review. They may also devote 16 hours to a systems review.

For group study courses, credit will be granted in 0.2 increments once the first full hour has been obtained. Also, for interactive self-study credit courses, CPEs will are obtainable in 0.2 hour increments. If an activity is less than 10 minutes in length, it will not qualify for CPE.

Other Policies and Exemptions

All hours exceeding the 80 required during a reporting period carry forward to the next period. However, ethics hours do not carry forward to meet future ethics requirements. But they can be applied to the total hours requirement.

It is the responsibility of the licensee to demonstrate that the CPE program contributes directly to the licensee's professional competence.

The Board will not accept courses designed for the general public. Furthermore, courses not for CPAs or sales-oriented presentations of any kind are prohibited. Other prohibited courses also include programs restricted to policies and procedures of a particular company. And finally, programs presenting scientific and technical knowledge beyond the scope required for the practice of a CPA.

The AICPA ethics course completed as a requirement for original licensure does not qualify for CPE credit.

Individual licensees who fall into the categories listed below are automatically excepted from the CPE requirements of AICPA. However, to qualify for exemption, they must not offer their services to third parties.

Any individuals who have retired

Licensees who are presently unemployed

CPAs who have temporarily but willingly left the workforce

Persons who have listed their formal status as "inactive"

Formally active CPAs can request exemption from continuing professional education requirements for the following reasons:

Health issues and/or complications

Active-duty military service

Natural disasters of a sort which prevent completion of CPE requirements

Other similar circumstances of a sort which prevent adequate completion of CPE requirements

![Find Your Required CPA CPE Hours [State Chart]](https://static.wixstatic.com/media/cc6a19_ecac25efe1e746829a8cc0abcccecc66~mv2.avif/v1/fill/w_867,h_276,al_c,q_80,enc_avif,quality_auto/cc6a19_ecac25efe1e746829a8cc0abcccecc66~mv2.avif)

![CPA Classes Online [490+ Self-Study Credits]](https://static.wixstatic.com/media/cc6a19_49dc7446da9c4f75b5e793041a5fc0e8~mv2.avif/v1/fill/w_867,h_276,al_c,q_80,enc_avif,quality_auto/cc6a19_49dc7446da9c4f75b5e793041a5fc0e8~mv2.avif)

![How to Become a CPA [State Exam Requirements]](https://static.wixstatic.com/media/cc6a19_c24b5840c53e424292a96948f6c1440c~mv2.avif/v1/fill/w_867,h_276,al_c,q_80,enc_avif,quality_auto/cc6a19_c24b5840c53e424292a96948f6c1440c~mv2.avif)

Comments